At pi Ventures, we invest in companies addressing global problems through 10x disruptive technology innovation. The central challenge: identifying them early enough to matter, but not so early that neither technology nor market is ready.

This document consolidates 2 interconnected frameworks for thesis building, deal evaluation, and portfolio tracking: the Demand & Supply Resonance Map, the Market Centricity Framework, and their longitudinal application to a portfolio company trajectory.

This is Part 2 of a 3-part series. Kalai helped us develop & structure this into a comprehensive deeptech investment framework series. You can read Part 1 here.

PART 2: MARKET CENTRICITY FRAMEWORK

Understanding what early commercial activity actually tells you. A handful of pilots may represent genuine beachhead or scattered demand. The difference determines scaling strategy and investor support.

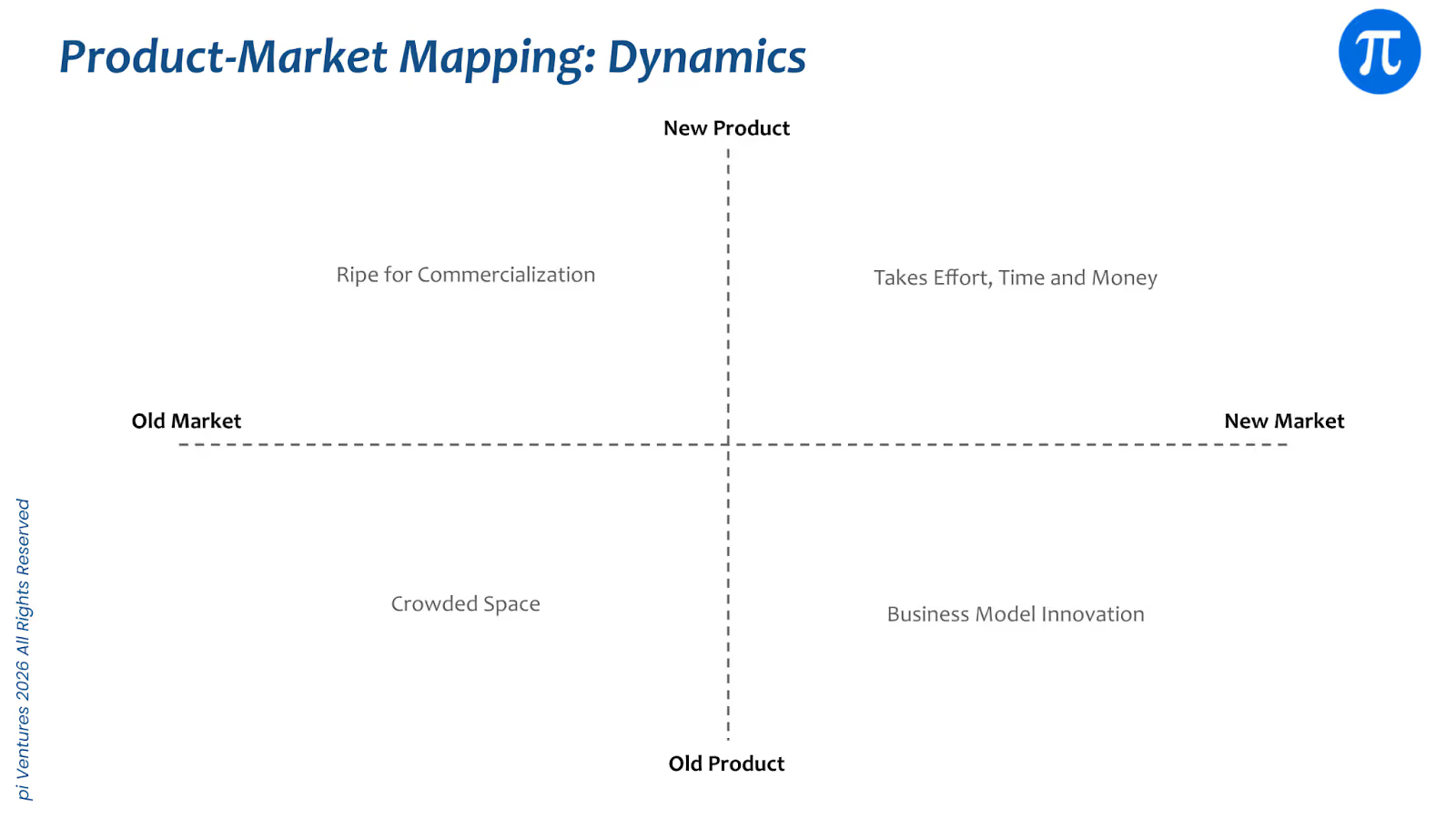

The Four Quadrants

Market Centricity maps startups across two dimensions: product maturity (new vs. existing variant) and buyer maturity (established vs. new market). Most early-stage startups might fall in one or more quadrants, and they might choose one primary quadrant for initial traction and then expand across quadrants over time.

Quadrant 1: Existing Market (Old Product, Old Market)

Competition on performance, price, or feature. Incumbent advantage. Scaling requires significant capital. Risk: feature matrix parity without defensible moat. Best for teams with deep operational efficiency.

Example: Another industrial robotics arm manufacturer selling into automotive plants. Buyers understand the category. Decision hinges on precision, uptime, and cost. Winning requires distribution and service scale, not a breakthrough tech.

Quadrant 2: Re-segmented Market (New Product, Old Market)

New product serving established buyers with proven need. Incumbent exists as reference architecture. Commercial risk is low relative to tech risk. Beachhead quadrant for most deeptech companies. Revenue validates technology.

Example: A new battery chemistry sold to EV OEMs. OEMs already procure batteries at scale. The startup must prove energy density, cycle life, and safety. If validated, displacement is viable. Market demand is not the question. The question is whether the technology delivers a step-change in value to the buyer (performance, cost, reliability, or safety etc to the OEM) and if there are enough advantages for the buyer to switch.

Quadrant 3: Re-invented Market (Old Product, New Market)

Existing technology reaches new buyers through new distribution, pricing, or business model. Risk: buyers may need different product features; old incumbent baggage becomes liability. Suitable when core tech is proven and scaling.

Example: Computer vision models originally built for autonomous vehicles repackaged as SaaS for retail analytics. The core tech exists. The buyer, pricing, and deployment model change. Execution risk shifts to integration and channel.

Quadrant 4: Invented Market (New Product, New Market)

Genuinely new product for genuinely new buyer. No prior procurement category. Buyer ecosystem nascent. Revenue model in design phase. Highest optionality but thinnest market signals. Risk: demand may not materialise. Only viable after the beachhead quadrant establishes proof.

Example: In-space manufacturing of pharmaceuticals in microgravity. No established procurement category. Buyers are exploratory biotech teams. Demand depends on proving materially superior molecular outcomes.

Beachhead Clarity Matters

Most early-stage companies should ideally anchor in one primary quadrant for initial traction, even if edges overlap. The framework clarifies where real commercial proof is emerging. Strong indicator: depth of fit, not market size.

Key question: Which specific cluster of buyers would be most disrupted if this product became unavailable tomorrow? A founder naming buyers and describing embedded workflows is describing a real beachhead. A founder naming market category is describing an aspirational target.

Behaviors of deep fit: Reference without asking, defend in procurement conversations, surface new use cases, resist switching even at lower price.

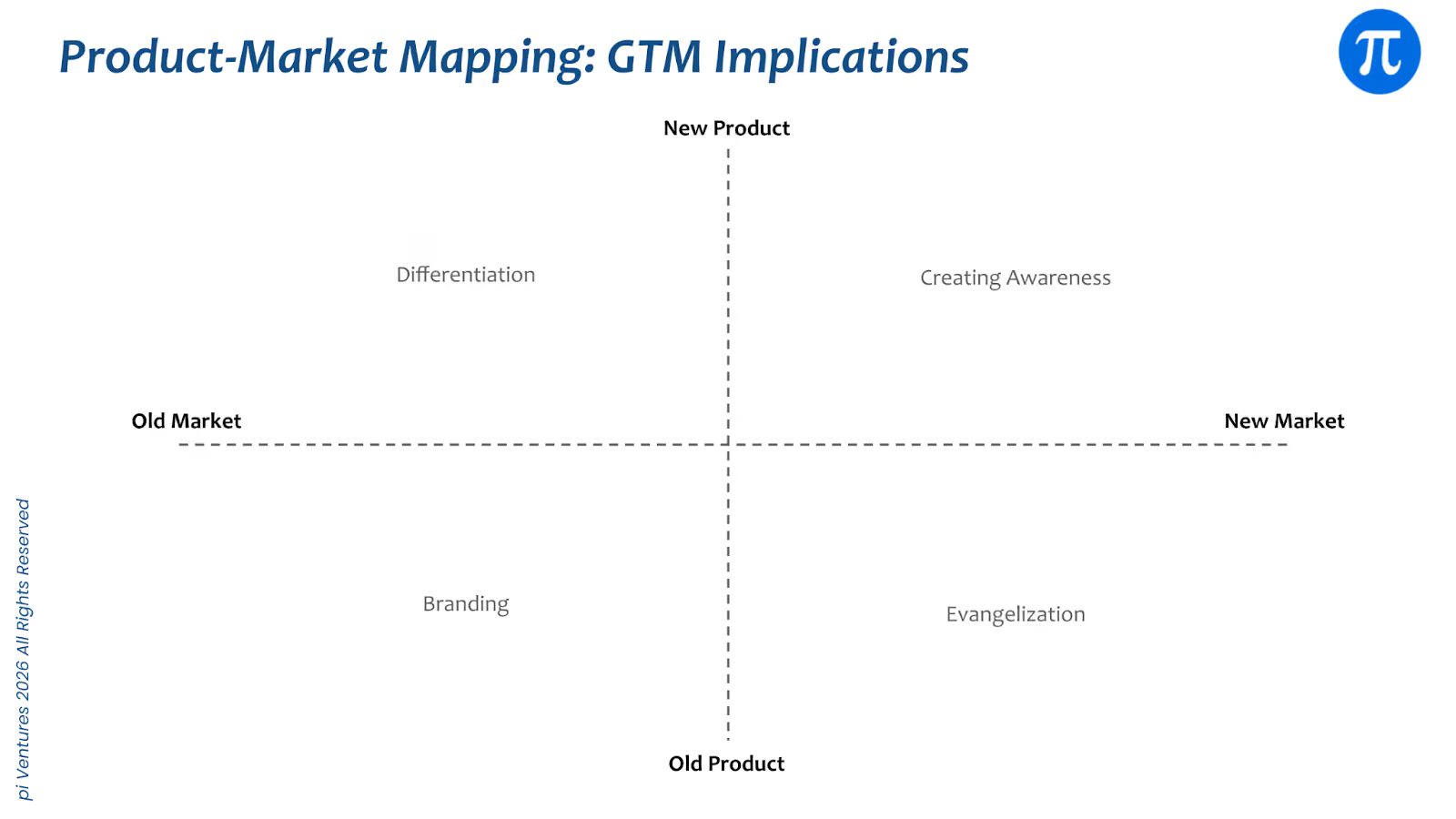

Go-to-Market Approaches by Quadrant

Different quadrants favour different GTM motions. Mismatch is a common failure mode.

- Re-segmented (Q2): Competitive displacement. Land with technical proof (benchmarks, early deployments). Expand through ROI conversations. Build with reference customers.

- Invented (Q4): Education and category creation. Land through pilot discovery. Expand through use case evangelism. Buyers are learning alongside the company.

- Re-invented (Q3): New distribution partnerships. Existing product wrapped in new pricing/model. Land through channel or white-label. Risk is integration overhead.

- Existing (Q1): Competitive positioning. Land through superior execution or lower cost. Expand through account density.

The Expansion Arc

Durable deeptech companies often follow a pattern: enter Re-segmented Market with new product serving existing buyer, build proof and moat, then discover Invented Market enabled by the same platform but structurally inaccessible to old technology.

- Phase 1: Re-segmented Entry: Existing demand + real incumbent = validation. Product fits specific context better. Early revenue funds platform maturation. Reference architecture established.

- Phase 2: Invented Market Expansion: Same platform reaches demand with no prior solution. Unlocks materially larger TAM. Regulatory credibility and data from Phase 1 enables Phase 2.

- Phase 3: Re-invented Adjacencies: Platform reaches new buyer segments through new distribution or financial structures not viable in early phase.

Low-Churn Verticals: Attractive but Structural Barriers

Healthcare, banking, defence, heavy industrial process control offer compelling economics once established (near-100% retention, large contract values, in-account expansion). But switching costs are operational, regulatory, interpersonal, not just contractual.

Entry approaches that work: Greenfield opportunity (new regulatory requirement, new department, new geography) where startup proves value before displacement question arises. Or complementary product strategy entering alongside incumbent as add-on before becoming primary.